How to Build a White Label Payment Aggregator Platform?

Every PSP founder and fintech operator eventually arrives at the same crossroads:

We have the merchant base. We have the transaction volume. We have the regulatory appetite. What we do not have is a payment aggregation platform we actually own. Every SaaS aggregator we looked at clips our margins, limits our routing logic, and holds our merchant data hostage. Building from scratch sounds like 18 months and $3M. There has to be a better path.

There is. And in 2026, that path is faster, more defined, and more accessible than it has ever been.

A white label payment aggregator platform gives you the full capabilities of a production-grade aggregation stack — multi-acquirer routing, merchant onboarding, split settlement, compliance layer — deployed under your brand, with your source code, on your infrastructure. This is not a SaaS license. It is not a reseller agreement. It is the actual infrastructure, owned by you, operated by you, scaled by you.

What Is a White Label Payment Aggregator Platform

A white label payment aggregator platform is a fully branded, source-owned payment aggregation infrastructure that a PSP, fintech, or digital bank deploys under its own identity.

It differs from both a payment gateway and a SaaS aggregator in a critical way:

| Layer | Payment gateway | SaaS aggregator | White label aggregator |

|---|---|---|---|

| Brand | Yours | Yours | Yours |

| Source code | Vendor-held | Vendor-held | Yours |

| Merchant onboarding | Not included | Vendor-managed | Yours |

| Routing logic | Vendor-controlled | Vendor-controlled | Yours |

| Settlement engine | Vendor-managed | Vendor-managed | Yours |

| Token vault | Vendor-held | Vendor-held | Yours |

| Compliance layer | Vendor-managed | Vendor-managed | Yours |

| Per-transaction fees | Yes | Yes | None after build |

The white label model is the only model in which you own the entire stack — not just the interface layer on top of someone else’s infrastructure.

Why Build a White Label Aggregator in 2026

The market case is straightforward.

The global payment aggregator market stands at USD 8.22 billion in 2026 and is growing at 18% CAGR to an estimated USD 24.65 billion by 2035. The embedded finance market — which white label aggregators power — is projected to reach USD 454.48 billion by 2031.

At the same time, the cost of NOT owning your aggregator compounds with every transaction. A platform processing $50M/month through a SaaS aggregator at a 0.2% platform fee incurs $100,000/month — or $1.2M/year — in fees for infrastructure it does not own. Over three years, that is $3.6M, for which there is nothing on the balance sheet.

Source-owned white label aggregator infrastructure converts that ongoing liability into a one-time capital investment — after which every basis point of improvement goes directly to P&L.

| Scenario | 3-year cost | What you own |

|---|---|---|

| SaaS aggregator at 0.2% on $50M/month | $3.6M+ | Nothing |

| White label build (one-time) | $500k–1.5M | Full source code, full stack |

| Difference | $2.1M–3.1M saving | Plus full ownership |

Read more about Why PSPs Are Moving Away From Stripe To Own Infrastructure

The Core Architecture: What a White Label Aggregator Actually Is

A serious white label payment aggregator is not a gateway with extra features bolted on. It is a ledger-centric orchestration platform — an event-driven financial system in which every transaction, settlement, and payout is recorded as an immutable ledger event and reconciled in real time.

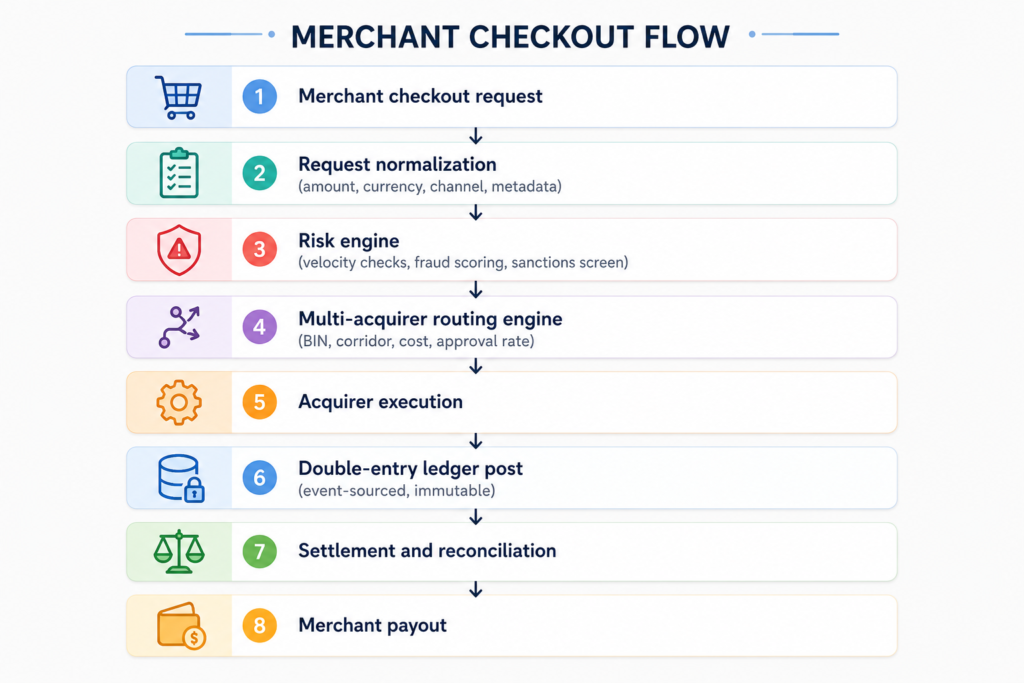

High-level transaction flow

Every step is a distinct microservice with its own domain boundary, independently deployable, horizontally scalable.

Module-by-Module Build Guide

Module 1: Merchant onboarding and KYB engine

The merchant onboarding engine is the front door of your aggregator. It handles everything from initial merchant application to live transaction processing authorization.

What it must include:

- API-first onboarding form with document collection

- Automated KYB (Know Your Business) workflows — company verification, director checks, beneficial ownership mapping

- Risk tiering engine — classify merchants by MCC, transaction volume, chargeback history, and geography

- Configurable approval rules — automatic approval for low-risk, manual review queue for elevated risk

- Merchant portal — real-time dashboard for transaction history, settlement status, and dispute tracking

- Onboarding webhooks — notify downstream systems on merchant status changes

| Risk tier | Typical profile | Processing limit | Review type |

|---|---|---|---|

| Tier 1 | Low-risk, established business | Standard | Automated |

| Tier 2 | Mid-risk, newer business | Capped | Manual review |

| Tier 3 | High-risk MCC (travel, gaming, crypto) | Restricted | Enhanced due diligence |

| Blocked | Sanctioned entity or prohibited MCC | Zero | Rejected |

Architecture note: Onboarding must integrate with your sanctions screening engine in real time. Every merchant application is screened against OFAC, UN, EU, and local watchlists before approval.

Read more about PSP & Aggregator Software Development

Module 2: Multi-acquirer routing engine

The routing engine is the commercial heart of your aggregator. It determines which acquirer processes each transaction — and that decision directly affects approval rates, processing costs, and ultimately, your margins.

Routing dimensions:

| Routing type | Logic | Business impact |

|---|---|---|

| BIN-based routing | Route by card issuer country, card scheme | Reduce cross-border decline rates |

| Cost-based routing | Route to lowest-cost acquirer for each transaction type | Optimize processing costs |

| Approval rate routing | Route to acquirer with highest historical approval rate for this BIN | Maximize revenue |

| Corridor routing | Route by origin/destination geography | Cross-border optimization |

| Fallback routing | Auto-retry on decline via secondary acquirer | Recover failed transactions |

| Load balancing | Distribute volume across acquirers to manage concentration risk | Operational resilience |

Why multi-acquirer routing matters at scale:

A platform processing $50M/month with a single acquirer at a 92% approval rate leaves $4M/month in declined transactions on the table. Adding a second acquirer with complementary BIN coverage can recover 2–4 percentage points of approval rate — a $1–2M/month revenue improvement.

The routing engine must be configurable without a code deployment. Business rules, routing weights, and acquirer priorities should be adjustable through an admin interface, not a developer ticket.

Module 3: Split payment and revenue share engine

The split payment engine is what separates a payment aggregator from a simple payment gateway. It automatically divides each transaction amount according to configurable rules — capturing your platform fee and routing the merchant’s net amount to settlement.

Split configurations:

| Split type | Use case | Example |

|---|---|---|

| Platform fee capture | Standard aggregator model | Platform takes 0.5%, merchant receives 99.5% |

| Marketplace split | Multiple sellers per transaction | Order split across vendors A, B, C |

| Partner commission | Referral or reseller network | 30% to introducing partner |

| Escrow hold | Marketplace, dispute protection | Funds held until delivery confirmation |

| Dynamic MDR | Volume-based pricing tiers | Large merchants pay lower effective rate |

Every split configuration must feed into the double-entry ledger simultaneously — not as a post-processing step. Splits that are calculated after the fact create reconciliation gaps.

Module 4: Event-driven settlement ledger

The settlement ledger is the source of financial truth for your entire platform. Every transaction, fee, payout, reversal, and adjustment is recorded as an immutable event — a permanent, auditable record that can be replayed to reconstruct any balance at any point in time.

Ledger architecture requirements:

- Double-entry accounting — every debit has a corresponding credit; the ledger always balances

- Event sourcing — transaction state is derived from an append-only event log, never mutated

- Idempotency — every ledger write is idempotent; duplicate events do not create duplicate records

- Multi-currency — ledger must support simultaneous balances in multiple currencies with FX conversion events

- Real-time — balance updates must be visible within milliseconds of event creation

- Audit-ready — immutable log with user attribution, timestamps, and change history

| Ledger event type | Triggered by |

|---|---|

FUNDS_CAPTURED | Successful acquirer authorization |

PLATFORM_FEE_DEDUCTED | Split engine on capture |

MERCHANT_LIABILITY_CREATED | Split engine on capture |

SETTLEMENT_BATCHED | Scheduled settlement run |

PAYOUT_INITIATED | Settlement engine |

PAYOUT_CONFIRMED | Bank rail confirmation |

CHARGEBACK_RECEIVED | Acquirer notification |

CHARGEBACK_RESERVE_HELD | Risk engine |

REFUND_INITIATED | Merchant or platform action |

Read more about How to Build a T+0 Real-Time Settlement Engine

Module 5: PCI-aligned tokenization vault

The tokenization vault stores sensitive payment credentials — card numbers, bank account details, wallet identifiers — as non-sensitive tokens. The vault is what enables recurring billing, saved payment methods, and cross-platform credential portability without storing raw card data.

Vault requirements:

- PCI DSS Level 1 certified infrastructure

- Format-preserving tokenization (tokens that match the format of the original data)

- Multi-asset support — cards (PAN), bank accounts (IBAN/account number), wallet identifiers

- Token lifecycle management — creation, rotation, expiry, deletion

- Network tokenization support — Visa Token Service (VTS) and Mastercard Digital Enablement Service (MDES)

- Role-based access controls — only authorized services can detokenize

Critical design principle: The vault must be isolated from all other platform services behind its own API boundary. No service has direct database access to raw credentials — all access goes through the vault API with full audit logging.

Module 6: 3DS2 orchestration

3D Secure v2 is mandatory for any white label aggregator operating under PSD2/PSD3 in Europe or seeking to minimize chargebacks globally. A native 3DS2 implementation — rather than a passthrough to a third-party ACS — gives you full control over authentication decisions.

3DS2 orchestration capabilities:

- Native 3DS2 request construction and response handling

- Frictionless flow optimization — use exemptions (TRA, low-value, recurring) to skip step-up authentication for low-risk transactions

- Step-up handling — seamless redirect to issuer ACS for challenge flows

- Intelligent exemption engine — automatically claim the right exemption based on transaction risk score, amount, and history

- Liability shift management — track which transactions carry liability shift and which do not

Exemption hierarchy:

| Exemption | Condition | Friction |

|---|---|---|

| Low-value | Under €30 / local equivalent | None |

| Transaction Risk Analysis (TRA) | Low fraud rate + risk score | None |

| Trusted beneficiary | Merchant whitelisted by cardholder | None |

| Recurring | Subsequent payment in series | None |

| Step-up required | High risk, no exemption applicable | Cardholder challenge |

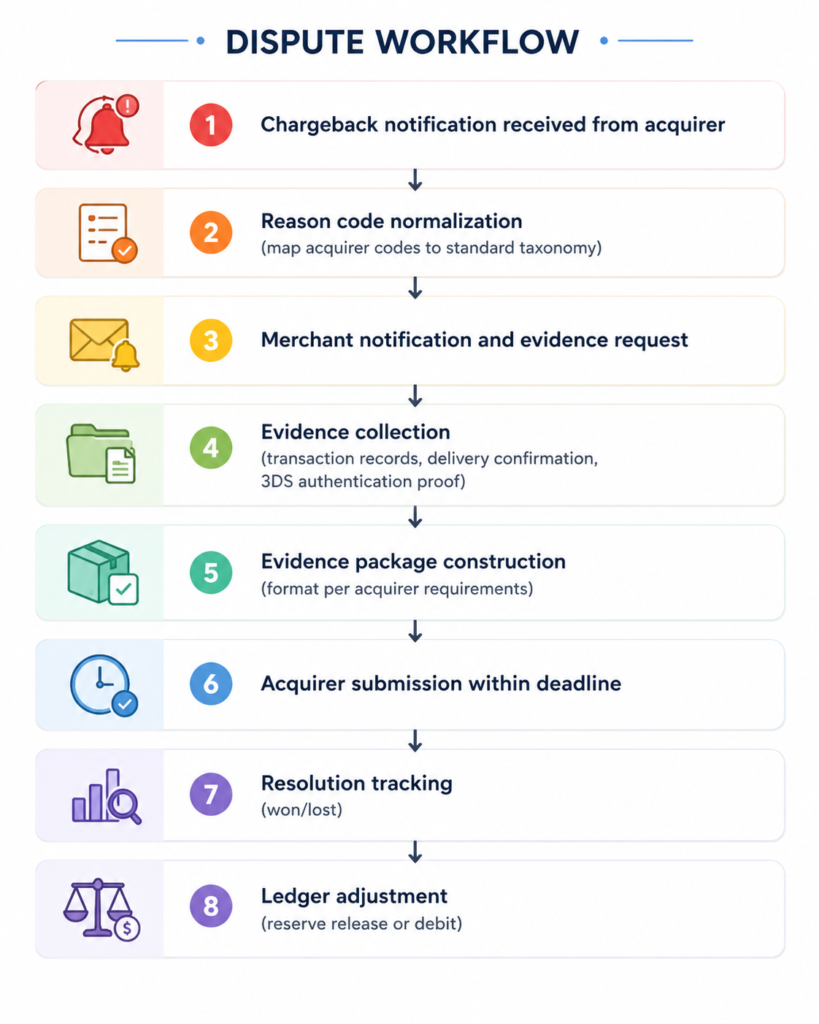

Module 7: Chargeback and dispute management

Chargebacks are the operational reality of payment aggregation. A white label aggregator must handle the full dispute lifecycle — from initial notification through evidence submission to final resolution — across multiple acquirers, each with their own reason codes, timelines, and evidence requirements.

Reserve management: Every merchant should have a rolling reserve balance — a percentage of processed volume held back to cover potential chargebacks. The reserve engine must calculate reserves in real time and release them on schedule.

Module 8: Payout and reconciliation engine

The payout engine disburses settled funds to merchants across whatever payment rails they require — bank transfer, instant payment, wallet credit, card push. The reconciliation engine ensures that every payout matches the corresponding ledger balance and acquirer settlement statement.

Payout modes:

| Mode | Settlement time | Use case |

|---|---|---|

| Standard batch | T+1 or T+2 | Default for most merchants |

| Same-day | Intraday cut-offs | Premium merchants |

| Instant payout | Real-time (fee-based) | On-demand for urgent needs |

| Scheduled | Custom calendar | Marketplace, subscription platforms |

Reconciliation flow:

- Ingest acquirer settlement files (MT940, CAMT.053, CSV, API)

- Match each acquirer record to internal ledger events

- Flag unmatched items for exception handling

- Calculate net settlement amounts per merchant

- Trigger payout run

- Mark ledger entries as settled

- Generate audit-ready reconciliation reports

Read more about How to Build a Reconciliation Engine

Compliance Architecture: Embedded by Design

Compliance is the foundation of a white label aggregator — not a feature layer added at the end. Platforms that bolt compliance on after build typically spend more on remediation than they would have on proper architecture from day one.

The minimum compliance stack

| Layer | Components |

|---|---|

| Identity and KYB | Document verification, liveness detection, beneficial ownership mapping, sanctions screening |

| Transaction monitoring | Velocity rules, AML pattern detection, high-risk MCC flagging, automated SAR generation |

| Sanctions screening | Real-time OFAC, UN, EU, and local watchlist checks on all onboarding and transactions |

| PCI DSS | Tokenization vault, network segmentation, key management, quarterly scans |

| Audit trail | Immutable event log with user attribution, timestamps, and role-based access controls |

| Data protection | GDPR/regional data residency, encrypted at rest and in transit, right to erasure workflows |

| Regulator reporting | Transaction reports, FIU filings, suspicious activity reports |

Global regulatory frameworks

| Jurisdiction | Framework | Key requirement |

|---|---|---|

| India | RBI PA-O, PA-P, PA-CB | Net worth ₹25 crore, escrow accounts, KYC, audit trail |

| EU | PSD3, EMI license | Safeguarding, SCA, DORA compliance |

| UK | FCA payment services | Capital adequacy, safeguarding, reporting |

| UAE | CBUAE payment institution | Capital requirements, AML/CFT compliance |

| Singapore | MAS Payment Services Act | Licensing tiers, safeguarding, AML/CFT |

| US | State MTLs | State-by-state money transmitter licenses, surety bonds |

Read more about Building a Payment Aggregator for the Middle East and Africa

How PrimeFin Labs Builds White Label Aggregators

PrimeFin Labs delivers source-owned, compliance-embedded white label payment aggregator infrastructure for PSPs, fintechs, digital banks, and SaaS platforms.

Every module is delivered as source code — not a SaaS key, not an API access credential. You own it, you host it, you modify it.

What PrimeFin Labs delivers

| Module | Delivery |

|---|---|

| Merchant onboarding and KYB | Automated verification, risk tiering, document validation — your code |

| Multi-acquirer routing engine | BIN-based, cost-based, corridor-based, fallback routing — your code |

| Split payment and revenue share engine | Dynamic splits, platform fee capture, partner commissions — your code |

| Settlement and payout orchestration | Any schedule, any currency, any rail — your code |

| PCI-aligned tokenization vault | Cards, accounts, wallets — your code |

| 3DS2 orchestration | Native authentication, intelligent exemptions — your code |

| Event-driven settlement ledger | Double-entry, event-sourced, real-time — your code |

| Chargeback and dispute management | Automated workflows, evidence handling — your code |

| Reconciliation engine | Acquirer file parsing, exception handling, audit reports — your code |

| Compliance layer | KYC/AML, sanctions screening, audit trails — your code |

| Admin and merchant dashboards | Real-time analytics, role-based access — your code |